Robin Roberts (and WheelsWithinWales) writes…

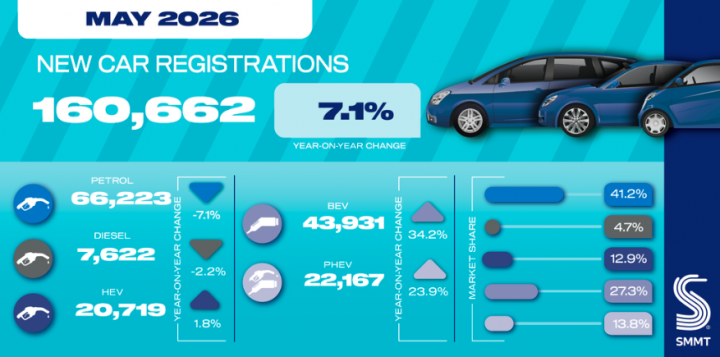

The UK’s new car market delivered its strongest May performance since before the pandemic, with registrations rising 7.1% to 160,662 units, reported the Society of Motor Manufacturers and Traders.

The performance was the best recorded for the month since 2019, although still -12.6% behind pre-pandemic levels.

Registrations in Wales last month rose 6.95% to 5,152.

A resurgence in private buyers drove the increase, with registrations up 17.2% as consumers responded to increasingly competitive offers from an unprecedented range of brands and a 6.4% increase in model choice – including a 25.6% uplift in BEV products year to date.

Fleet demand grew more modestly, rising 1.8% but still accounted for more than half (57.1%) of all registrations. The smaller business sector declined -18.8%, although in volume terms the drop was marginal (720 units).

| May top ten UK | May top ten Wales | |

| Ford Puma

Kia Sportage Vauxhall Corsa Jaecoo7 Nissan Qashqai VW Golf Mini Cooper VW Tiguan Vauxhall Frontera Hyundai Tucson |

MG HS

Ford Puma Kia Sportage Nissan Qashqai Vauxhall Corsa Volvo XC40 Hyundai Tucson MG ZS VW Golf Jaecoo7 |

The gradual shift in consumer demand for new technologies continues to reshape the market. Registrations of petrol and diesel cars fell by -7.1% and -2.2% respectively, as electrified vehicles gained ground.

Hybrid electric vehicle (HEV) uptake rose 1.8% and plug-in hybrid deliveries grew 23.9% to take an enlarged 13.8% market share. Battery electric vehicle (BEV) uptake, meanwhile, increased 34.2% to take 27.3% of the market, the highest recorded so far in 2026.

The uplift reflects both expanding model choice and sustained competition, particularly in the electric vehicle market where substantial manufacturer discounting continues to play a significant role in driving uptake.

Government support, including the Electric Car Grant, has also helped stimulate demand, alongside rising consumer interest amid wider economic and geopolitical uncertainty.

Despite recent momentum, however, the transition to zero-emission mobility remains well behind the mandated trajectory. Year-to-date, BEVs account for just 23.9% of the market, well short of the 33% required in 2026.

While various flexibilities can be drawn upon to help meet the regulation, this widening gap between mandated targets and consumer demand is increasing pressure on manufacturers which must try to absorb the rising costs of compliance.

In the seventh Carbon Budget, published this week, Government envisages EVs comprising 95% of the new UK car and van market by 2030 – an ambition well beyond the targets set by the mandate of 80% for cars and 70% for vans. If such targets are to be credible and a tripling of EV demand in three years is highly unlikely under current outlooks then equally ambitious fiscal and investment support would be essential.

A holistic review of the transition is urgently needed, therefore, else the investment proposition of the UK is undermined, consumer choice constrained, and the pace of fleet renewal – essential to cutting road transport emissions – curtailed.

Mike Hawes, SMMT Chief Executive, said, “Britain’s car buyers are responding to a market offering more choice than ever, from both new and familiar brands, resulting in a robust May.

The EV transition is progressing, but consumer uptake still lags behind even today’s targets, let alone the ambition set out in the latest Carbon Budget. While industry shares the long-term ambition, the pathway to Net Zero must be credible.

It cannot come at the cost of lost competitiveness and deindustrialisation. A review of the transition is now urgent to ensure ambition matches market realities and we have a sustainable path to road transport decarbonisation.”

The new light commercial vehicle (LCV) market rose 3.6% in May with 23,620 vans, pickups and 4x4s joining UK roads.

The performance marks a second successive month of growth for the first time since 2024.

Overall growth was driven by increased demand for large vans, with registrations up 18.6% to 17,380 units and a market share of 73.6%, compared with a 64.3% share in May last year. Uptake of 4x4s also grew, up 16.2% to 832 units, while deliveries of medium and small vans fell by -7.5% and -24.5% to 3,762 and 508 units respectively.

Demand for pickups fell sharply for an eighth month, down -57.7% to 1,138 registrations, now representing just 4.8% of the total market versus 11.8% a year ago.

The decline reflects the ongoing impact of fiscal changes introduced for double-cabs last April, which classify them as cars for Benefit in Kind purposes with significant cost implications for vital business sectors such as farming and construction.

Industry continues to call on government to reverse this measure to encourage investment into lower emission and zero emission models, supporting decarbonisation while still benefiting Treasury revenue.