Hasn’t the world got enough SUVs already? – asks Dave Moss.

Though long-targeted over weight, fuel consumption, aerodynamics and emissions, Sport Utility Vehicles and their crossover cousins have become a surprising success story. Morphing out of practical 1980’s 4×4 estate-car type “dual purpose” workhorses like early Landcruisers, Range Rovers and Patrols, the 1988 Land-Rover Discovery (like the vehicle in the heading photograph, above) was probably the SUV’s earliest recognisable ancestor – until four-wheel-drive downsizing began in earnest, bringing us assorted 1990’s Fronteras, Mavericks, Terranos, and the original, Karmann-built Kia Sportage.

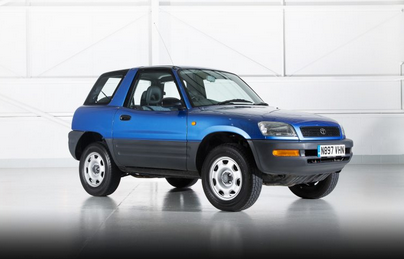

Then, suddenly, in 1994, Toyota’s nimble new 3 door RAV 4 rolled onto their home turf – a more stylish, car-oriented “crossover” which looked better, drove better, and was more comfortable – if short on interior space. Five-door versions soon addressed that, and simultaneously undercut the old school’s prices by well over £2000. Though still offering permanent four wheel drive, the RAV4 cast aside agricultural connections, leaf springs, locking differentials and transfer gearboxes, edging into position as a low key but trend-starting mould-breaker. Six years on, in 2000, when, tellingly, the average Co2 emissions of so called “Dual Purpose” vehicles was 260g/km, just 29,185 examples were sold in Europe, and 138,669 across the globe.

Though joined in the 1990’s by Honda’s CR-V, and other vehicles developed along similar lines in the early 2000’s, ten years on from the RAV 4’s launch in 2004, the best sellers list in a near-record UK market of 2,567,269 cars still comprised…. ten familiar mainstream hatchback models. The SMMT reported 179,439 “Dual purpose 4×4” sales, taking 7% of the market, while the RAV 4 had matured gently, with just over half a million European sales in ten years – but now, something was definitely stirring… for 111,234 of those – 20% – left the showrooms in 2004 alone.

In 2006, Nissan bravely sidelined its “conventional” Almera and Primera ranges to slot in the new Qashqai, an adventurous, chunkily styled crossover. By 2010, buoyed by improving financial packages, sales of increasingly stylish, high-riding – if sometimes bulky – lifestyle-oriented vehicles were forging ahead – and the Qashqai became the first Nissan to reach Britain’s top ten best sellers since 1983. Two years later, ACEA figures revealed Europe-wide sales of 1,614,491 SUV’s – 13% of the market, though still dwarfed by the 45% share taken by 5.448 million combined small/medium A, B and C sector sales.

After this, must-have mindsets began driving a seemingly unstoppable bandwagon. By 2017, sales had doubled in just five years, and 3,644,097 SUV’s found European homes, equivalent to almost 60% of Europe’s combined A, B and C sector sales – despite their total growing to 6.24 million units. The SMMT recorded 460,412 British SUV sales – the only segment showing growth that year – again over double the 2012 figure – and over 18% of the 2,540,617 full year sales. Nissan must have been well pleased: 11 years from launch, the Qashqai’s 64,216 sales and 2.5% market share turned it into Britain’s fourth best selling car, and the only SUV in the 2017 top ten.

Since 2017, unpredictable events have pushed new car sales into uncharted territory. Automotive data analysts JATO declared January 2022 the worst sales month since 1991, with 811,332 new cars registered across 26 European markets. Only two sectors showed signs of life: Electric Vehicles… and SUV’s, with 402,900 sales accounting for 49.7% of the European market – their highest ever monthly share. This trend has become a global phenomenon, the SUV fleet having grown from an estimated 50 million vehicles in 2010 to around 320 million last year – equating to all the cars in Europe – and a further 10% sales uplift in 2022 has already added another 35 million units…

The International Energy Agency (IEA) estimates that SUV’s, including US RV’s and light trucks, accounted for over 45% of global car sales in 2021. It’s concerned that such vehicles rank amongst the top causes of carbon dioxide emissions growth over the last ten years, and estimates that over 98% of SUV’s still use internal combustion engines. Those extra 35 million units are calculated to increase annual Co2 emissions by 120 million tonnes, and the IEA also reckons that, since SUV’s are heavier than mid-sized cars, on average they consume around 20% more energy. Consequently, it says, reducing oil demand as electric vehicle numbers increase is being cancelled out by SUV sales growth.

Thus the IEA feels that global fuel economy has worsened since 2010, despite growing electric vehicle use – and efficiency improvements in smaller cars. It is calling for tailored government taxation policies to support a quicker shift towards electric vehicles – and incentives for early replacement of fossil fuel powered SUV’s. It also wants policy makers to monitor average vehicle sizes – pointing to “weighted” taxation measures already introduced in France and Germany on higher-emission cars… including SUV’s.

While agreeing that SUVs are usually bigger and heavier than hatchbacks and saloons, leading to 13% higher average volume-weighted emissions than traditional vehicles, JATO sees things differently. It says that light city-cars, and mainstream B and C segment models should now logically be leading the low emissions charge, but… SUVs have made better progress in reducing Co2 emissions than any other segment. It claims mid-size SUVs were the greenest vehicles in Europe in 2021, their average 65.4g/km emissions the lowest across 14 segments – resulting directly from new EV variants becoming available. In total, according to JATO data, of the 39 mid-size SUV models available in Europe last year, 28 – around 55% – were battery electric or plug-in hybrids, up from 45% two years ago – marking the first time the SUV “electrification rate” has come into line with non-SUV cars.

Perversely, however, the smallest, B- size SUV group posted the second highest average emissions among all SUV sub-segments. JATO believes this results from extreme customer price sensitivity, which makes electrification difficult for manufacturers unable to raise prices significantly. This is a fast-growing segment, currently the third largest in Europe, and JATO feels that manufacturers – not legislators – must address this issue sooner rather than later.

As motoring moves inexorably into an electrified future, experts appear undecided on whether SUV’s are a genuinely worrying “elephant in the showroom”. Even before decisions on a 2035 internal combustion engine phase-out were twinkles in political eyes SUV’s had long been regarded as environmentally undesirable, and a clear target But then, as the old saying goes… perhaps things aren’t always quite as they seem…